Pay Down Debt

If you have an outstanding credit card, student loan, or car finance debt, you probably can’t bear to look at the amount you’re paying for the interest rates alone. It can feel like you’re making zero progress when most of your repayments are paying off the interest, not the debt amount.

The solution? Pay more.

That’s probably not what you wanted to hear, right? You may be wondering, “How can I possibly save more by spending more?”

The simple truth is the faster you pay off your debt, the less interest you get charged in total.

Let’s say you have a $10,000 student loan outstanding at a 6.8% interest rate and a 10-year repayment period. Your standard monthly payments should be around $115 a month. But if you pay extra each month, you can save a lot.

Making just $100 extra payments each month could save a huge amount of interest. It could even cut it almost in half! If you can’t pay an extra $100, or $200 each month, even $20 a month can make a HUGE difference. See for yourself by calculating your savings using this calculator.

If you’re still having trouble getting out of debt, you may want to check out my article on how to get out of debt fast.

Set Money Rules for Yourself

We all work in different ways when it comes to money. There’s rarely any one-size-fits-all approach to spending, saving, and cutting expenses. So this is where setting money rules for yourself comes in.

If you know you have a particular bad money habit, set a rule for yourself to help avoid it. For example, if you’re an online shopping addict or an impulsive spender, a simple money rule could be to always wait 24 hours before making a purchase if it’s over a certain amount.

Maybe you also put away the same amount you spend into a separate savings account. That way, you’re down double the money. So the next time you want to buy something, you’ll think twice about it.

Setting rules for yourself is the best way to curb your bad habits and reward your good ones.

Money-Saving Strategy #2: Earn More Money

Cutting your expenses is a great start. But remember, while there’s a limit to how much you can cut, there’s no limit to how much you can earn.

Before you roll your eyes and skip this step, it is ALWAYS possible to earn more. Even if there’s a recession, even if you’re broke, busy, or don’t know where to start.

The good news is that there are several ways to start earning more. You can ask for a raise at your current job, find a higher-paying job, start a business, or pick up freelance work. And, by the way, if you are worried about a recession, read what I said about protecting your money ahead of a potential recession in this recent article with Business Insider.

Negotiate a Raise

Many people will just take their salary, grumble quietly about it, and nothing changes. But did you know that one of the simplest ways to get more money is to… just ask for it?

With just a five-minute conversation, you can make thousands more, and what’s better, the gains add up year after year.

This is one of the best ways to make money through a single conversation. It’s essentially quick money that—unlike taking surveys or selling your body to medical studies—gives you a LOT of money over many years.

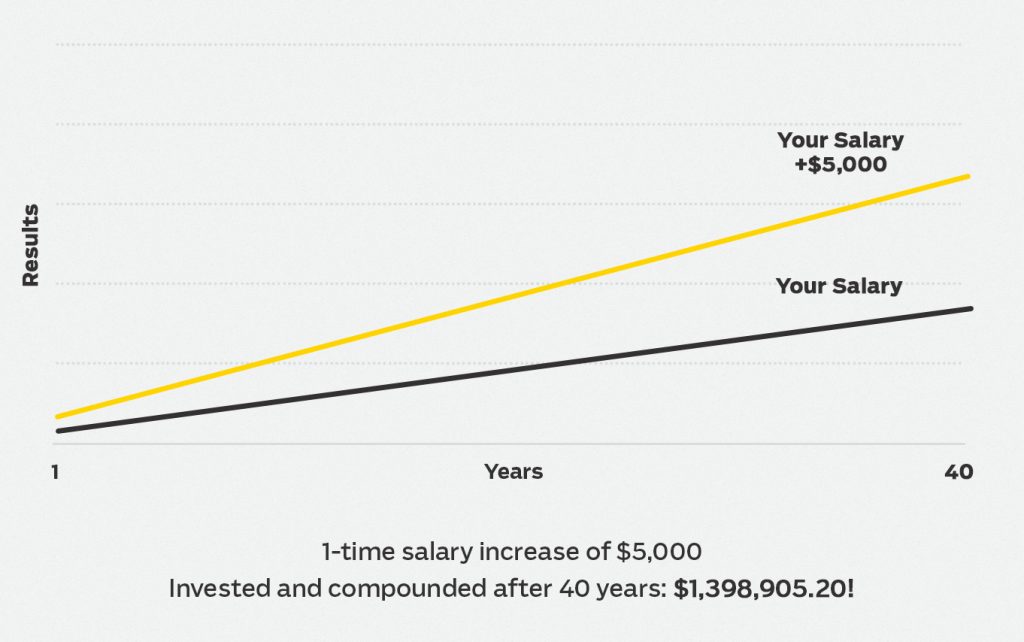

Check out this chart demonstrating the effects of ONE $5,000 raise:

For some actionable tips for negotiating your salary, check out this comprehensive post on how to negotiate your salary. It’s got a ton of information, and the steps are easy to follow.

Of course, it isn’t always that simple. Some bosses and industries have set salaries with minimal wiggle room. In that case, your next move is to…

Land a Higher Paying Job

If your boss isn’t interested in paying more money, the natural next step is to look elsewhere. Staying at a company for 10 or 20 years is a thing of the past for many people now. Sadly, loyalty and longevity at a company aren’t rewarded like they used to be.

So the next solution is to land a higher-paying job. But how?

Should you change jobs? Change industries? How do you know whether to stay put or to take a risky move that may result in more money?

If you find yourself in this situation, we have a ton of great resources on finding a better job on YouTube.

Start a Business or Freelance

Finding a new job or changing careers takes time. But in the next few days, you can set up your first side hustle. Once you get your first paying client, it’ll be easier to get more clients and make more money.

First thing: Many websites will tell you to troll for freelance gigs on places like Fiverr or Mechanical Turk. These places work if you want to compete with people all over the world in a race to do the most work for less. No thanks.

Instead, look at what you’ve already got. 95% of jobs can translate into some sort of side gig. Ask yourself:

- What do I enjoy?

- What do I do with my free time?

- What do people ask me to do because I’m so good at it?

Start by assessing the skills you use every day at home or work. Remember, people pay for solutions, not your skills. How can you take your skills and turn them into a solution for someone else’s problem?

Here’s a very simple example:

Skill: You’re good at math

Problem you can solve: With schools shut down in most states, many parents are struggling to help their kids with distance learning and would happily pay for tutoring

Your New Side Hustle: Tutoring kids in math over Facetime or Zoom

Now imagine if by tutoring for a few hours a week, you suddenly had an extra $500 a month.

That money can go straight to savings without reducing any of your spending. And this is just one small-scale example, it can work for virtually any skill. That’s why earning more is one of the best ways to save money.