Investing for Beginners: A Quick and Easy Guide to Investment

Investing is the single most effective way to get rich. But many of you mistakenly believe that investing is something complex and fancy requiring a huge chunk of your time.

It doesn't have to be! In this post, I'll take you through my beginners' guide to investing so that you can get started right now.

My Personal Take on Investing

In relationships and work, we want to be better than average. In investing, average is great.

So ignore the allure of flashy investment tactics that promise you overnight wealth. Average might sound boring and unsexy, but choose to be rich over sexy.

When it comes to investing, you just have to do these three simple things:

- Pick a low-cost index fund that tracks the S&P 500.

- Automate your investments every month.

- Let your money grow over time.

Once you've set these up, you can start following my Ladder of Personal Finance approach. (which I'll show you below)

The Benefits of Investing Early

Every year you wait to get started with investing, you miss out on thousands of dollars. Here's an example:

Dumb Dan invested for 20 more years than Smart Sally but is still behind by $50,000. Meanwhile, Smart Sally has $200,061 in just 10 years. She just started early and continued to invest over time.

To make sure you’re investing regularly, I recommend setting it up automatically, so you don’t need to think about doing it. This is the best way to take advantage of human psychology: we all get unmotivated, distracted, and forgetful. By setting up an automatic system, you’ll continue investing even when you’re busy or focused on other things.

The Ladder of Personal Finance

Each rung of the Ladder of Personal Finance builds on the previous one, so when you finish the first, go on to the second, and so on.

Wherever possible, I recommend automating every step as you go up the Ladder. If you can’t get to the sixth rung yet, don’t worry—do your best for now:

Rung #1: Contribute to your 401k

Each month you should be contributing as much as you need to in order to get the most out of your company’s 401k match. That means if your company offers a 5% match, you should be contributing AT LEAST 5% of your monthly income to your 401k each month.

A 401k is one of the most powerful investment vehicles at your disposal.

Here’s how it works: Each time you get your paycheck, a percentage of your pay is taken out and put into your 401k pre-tax.

This means you’ll only pay taxes on it after you withdraw your contributions when you retire.

Often, your employer will match your contributions up to a certain percentage.

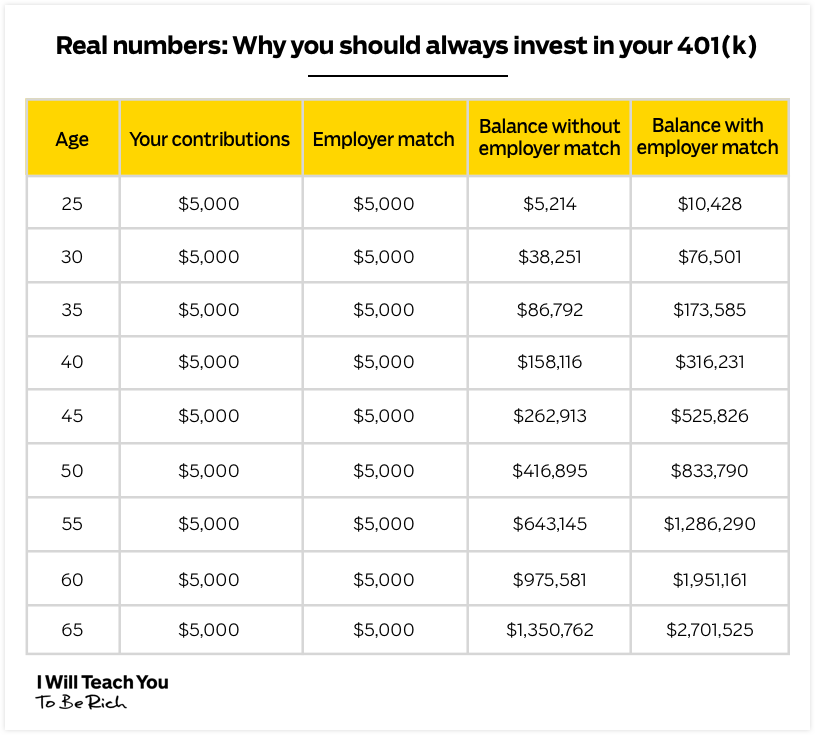

For example, imagine you make $150,000 per year and your company offers 3% matching with their 401k plan. If you invested 3% of your salary (around $5,000) into your 401k, your company would match your amount, effectively doubling your investment.

Here’s a graph showcasing this:

This, my friends, is free money (aka the best kind of money).

Not all companies offer a matching plan — but it’s rare to find one that doesn’t. If your company offers a match, you should at least invest enough to take full advantage of it.

Where’s my 401k money going?

You have the option to choose your investments when you put money into a 401k. However, most companies also give you the option to entrust your money with a professional investing company. They’ll give you a variety of investment options to choose from and can help answer any questions you have about your 401k.

The other great thing about a 401k is how easy it is to set up. You just have to opt in when your company’s HR department offers it. They’ll withdraw only as much as you want them to invest from your paycheck.

When can I withdraw money from my 401k?

You can take money out of your 401k when you turn 59 ½ years old. This is the beginning of the federally recognized retirement age.

Of course you CAN take money out earlier — but Uncle Sam is going to hit you with a 10% federal penalty on your funds along with the taxes you have to pay on the amount you withdraw.

That’s why it’s so important to keep your money in your 401k until you retire.

If you should ever decide to leave your company, your money goes with you! You just need to remember to roll it over into your new company's plan.

Rung #2: Pay off high-interest debt

Once you’ve committed yourself to contributing at least the employer match for your 401k, you need to make sure you don’t have any debt. If you don’t, great! If you do, that’s okay. I have 4 ways to help you get out of debt quickly.

Rung #3: Open a Roth IRA

Once you’ve started contributing to your 401k and eliminated your debt, you can start investing into a Roth IRA. Unlike your 401k, this investment account allows you to invest after-tax money and you collect no taxes on the earnings. There’s a maximum for how much you can contribute to your Roth IRA, so stay up to date on the yearly maximum.

Unlike a 401k, a Roth IRA leverages after-tax money to give you an even better deal. This means you put already-taxed income into investments such as stocks or bonds and pay no money when you withdraw it.

When saving for retirement, your greatest advantage is time. You have time to weather the bumps in the market. And over the years, those tax-free gains will prove an amazing deal.

Your employer won’t offer you a Roth IRA. To get one, you’ll have to go through a broker.

There are a lot of elements that can determine your decision, including minimum investment fees and stock options.

A few brokers we suggest are Charles Schwab, Vanguard (this is the one I use), and E*TRADE.

NOTE: Most brokers require a minimum amount for opening a Roth IRA. However, they might waive the minimum if you set up a regular automatic investment plan.

Where does the money in my Roth IRA get invested?

Once your account is set up, you’ll have to actually invest the money.

Let me say that again, once you set up the account and put money into it, you still need to invest your money.

If you don’t purchase stocks, bonds, ETFs, or whatever else, your money will just be sitting in a glorified savings account not accruing substantial interest.

My suggestion for what you should invest in? An index fund that tracks the S&P 500 and is managed with barely any fees.

For more, read my introductory articles on stocks and bonds to gain a better understanding of your options. Or, you can watch my deep dive into how you can choose a Roth IRA:

The world wants you to be vanilla... …but you don’t have to take the same path as everyone else. How would it look if you designed a Rich Life on your own terms? Take our quiz and find out: Take the Quiz

When can I withdraw money from my Roth IRA?

Like your 401k, you’re expected to treat this as a long-term investment vehicle. You are penalized if you withdraw your earnings before you’re 59 ½ years old.

You can, however, withdraw your principal, or the amount you actually invested from your pocket, at any time, penalty-free (most people don’t know this).

There are also exceptions for down payments on a home, education for you/partner/children/grandchildren, and some other emergency reasons.

But it’s still a fantastic investment to make, especially when you do it early. After all, the sooner you can invest, the more money your investment will accrue.

Rung #4: Max out your 401k

If you have money left over, go back to your 401k and contribute as much as possible to it (this is above and beyond the employer match). Maxing out your 401k before opening a non-retirement investing account is a good idea because you’ll pay less tax money on any 401k investments.

Rung #5: Invest in your Health Savings Account (HSA)

If you’ve completed Rung 4 and still have money left over, you can take advantage of your Health Savings Account (if you have access to one).

An HSA can double as an investment account with incredible tax features that few people know about.

What it is: An HSA is a place to set aside pre-tax money to pay for qualified medical expenses, including deductibles, copayments, coinsurance, and some other health-related expenses.

How it works: You contribute money to your HSA account. You then get a debit card to pay for qualified medical expenses using the money you’ve contributed.

So what? The money you put in the HSA is tax-free. So if you have medical expenses, you can pay for them with tax-free money.

But if you’re contributing thousands of dollars and not actually getting body scans and new glasses, you might think, “What’s the point?” Well, here’s something that not many people are aware of – the money you’ve saved can be invested! This is the real benefit.

You contribute tax-free money, take a tax deduction, AND grow it tax-free. It’s a triple whammy.

This account is typically overlooked and not understood, and it’s also only available if you have a high-deductible health plan.

If you completed the first 4 rungs, call your insurance provider or benefits manager and ask if you have a high-deductible health plan. If they say yes, ask if you can pair an HSA with your account.

Rung #6: Open a non-retirement investing account

If you have money left, open a regular non-retirement account and put as much as possible there. Also pay extra on any mortgage debt you have, and consider investing in yourself — whether it’s starting a side hustle or getting an additional degree, there’s often no better investment than your own career.

The Ladder of Personal Finance is pretty handy when considering what to prioritize when it comes to your investments.

Asset allocation: The most important thing in investing

401ks and Roth IRAs are the baseline investment vehicles you need to have.

If you want to start dipping your toes in building your own portfolio (collection of investment assets) beyond these investment vehicles, I want to introduce you to one key concept: Asset allocation.

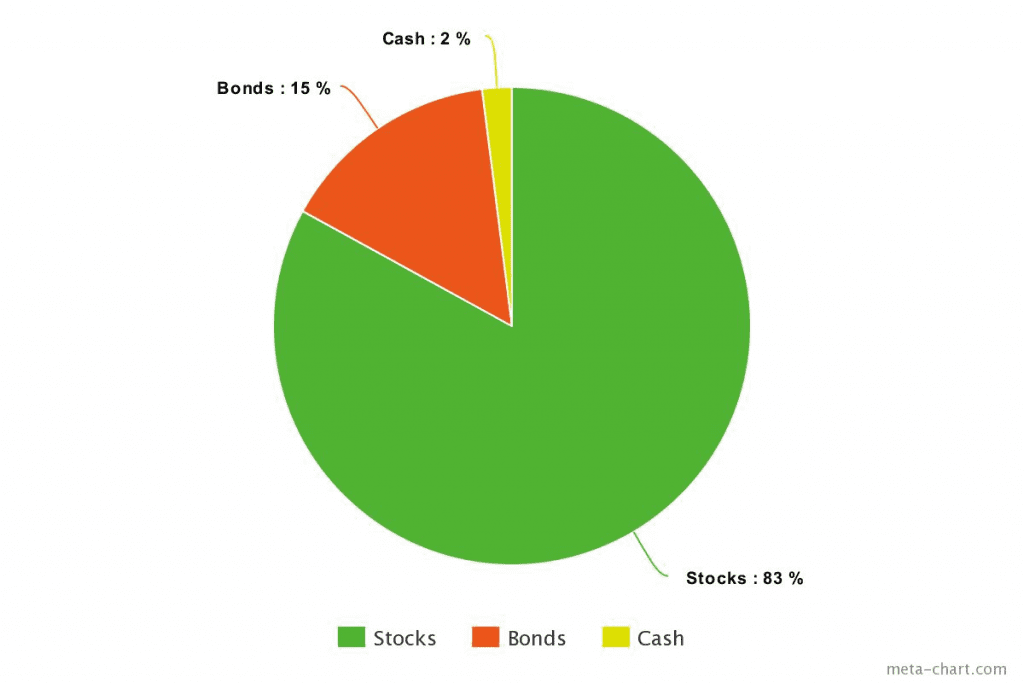

Here’s my portfolio:

Inevitably, whenever I’m teaching someone about the basics of investing, someone will pipe up with a myriad questions, like these:

- “What stocks should I buy?”

- “Is X company a good investment?”

- “Is $XX too much for this stock?”

Before you make an investment in any sort of stock, bond, or whatever, you need to understand that’s not nearly as important as asset allocation (i.e., what your pie looks like).

When you invest, you can do so by allocating your money across different asset classes. Though there are many different kinds of asset classes, the three most common ones are:

- Stocks and mutual funds (“equities”). When you own a company’s stock, you own part of that company. These are generally considered to be “riskier” because they can grow or shrink quickly. You can diversify that risk by owning mutual funds, which are essentially baskets of stocks.

- Bonds. These are like IOUs that you get from banks. You’re lending them money in exchange for interest over a fixed amount of time. These are generally considered “safer” because they have a fixed (if modest) rate of return.

- Cash. This includes liquid money and the money that you have in your checking and savings accounts.

When it comes to investing for beginners, a common mistake is investing in only one category. This is dangerous over the long term. This is where the all-important concept of asset allocation comes into play.

Remember it like this: Diversification is D for going deep into a category (e.g., stocks have large-cap stocks, mid-cap stocks, small-cap stocks, and international stocks). Asset allocation is A for going across all categories (e.g., stocks, bonds, and cash).

How much you allocate in each asset class depends completely on you and your risk tolerance. For example, if you’re young and have many years before you retire, you might want to invest more in things like stocks. But if you’re older and are close to retirement age, you want to hedge your bets as much as possible and go with safe investments like bonds.

You don’t want to keep all your investments in one basket. Keep your asset allocation in check by buying different types of stocks and funds to have a balanced portfolio—and then further diversify in each of those asset classes.

A 1991 study discovered that 91.5% of the results from long-term portfolio performance came from how the investments were allocated. This means that asset allocation is CRUCIAL to how your portfolio performs.

If you want some more solid examples of portfolio mixes, here's more information on asset allocation and diversification.

Stocks, CDs, and bonds

If you want to start getting into the weeds, there are a ton of different asset classes you can choose from and even more variety in individual investments you can make.

If you want to learn more about some of these investment options, be sure to check out my resources below:

- All about stocks and bonds

- All about mutual funds

- My Simple Retirement Guide (real life story inside)

FAQs about Investing for Beginners

What does it mean to invest early?

Investing early means starting to invest your money as soon as possible, ideally in your twenties or thirties.

Why is it important to invest early?

Investing early is important because it allows you to take advantage of compound interest, which can help your money grow exponentially over time. It also allows you to weather market fluctuations and take a long-term approach to your investments.

What are some benefits of investing early?

Some benefits of investing early include having more time to grow your investments and building wealth over time. This can help you achieve financial independence and reach your long-term financial goals.

What are the potential risks of investing early?

Investing always carries some level of risk, and investing early is no exception. Market volatility, economic downturns, and individual choices can all impact the performance of your investments. That’s why it’s so important to diversify your portfolio – and have a long-term perspective of your investments.

Stay in the know

Be the first one to receive new releases,

special offers, and more